Contents

Financial scams in the UK rarely start with a cartoon villain and a bag marked “cash.” They usually start with a polite call, a sharp website, a familiar logo, a cloned investment firm, a fake trading platform, or a message from someone who appears to know enough about markets to sound credible. The victim often realises something is wrong only when a withdrawal fails, a promised return disappears, or the “adviser” asks for one more payment to release funds.

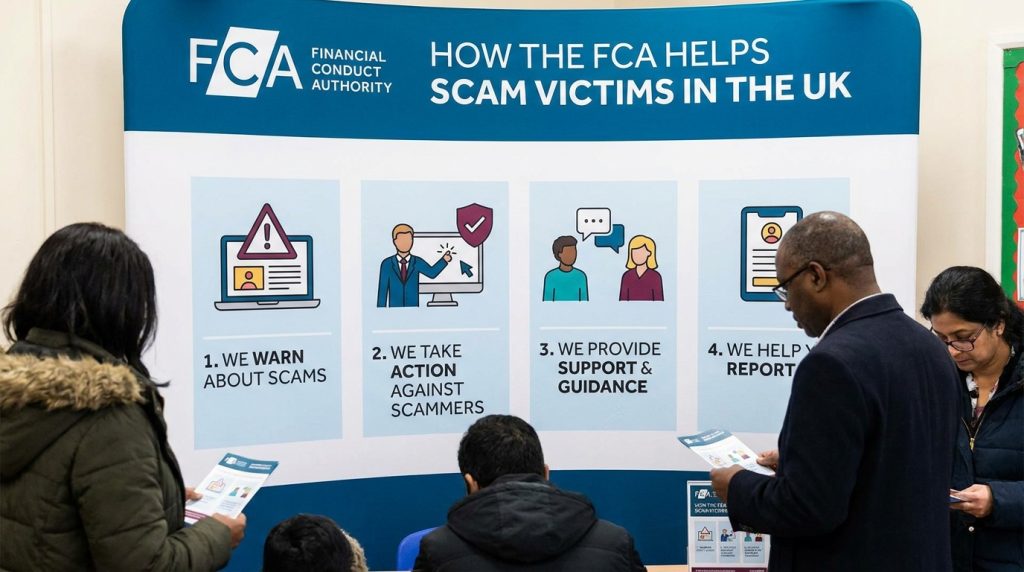

The Financial Conduct Authority, better known as the FCA, plays a central role in the UK’s response to investment scams and unauthorised financial firms. It is not a police force, and it does not act like a personal recovery agent. It will not usually phone the scammer and demand your money back by Friday, tempting though that image is. Its role is different. It regulates authorised financial firms, warns the public about unauthorised operators, takes enforcement action, shares intelligence, and helps consumers understand where to report fraud and where to seek redress.

For investors and traders comparing markets, brokers and financial products through resources such as Investing.co.uk, the FCA should be part of the basic safety process. Before money moves, the firm, product and contact details should be checked. After a scam, the same checks help establish whether the victim dealt with an authorised firm, a clone, an unauthorised business, or a criminal operation using financial language as cover.

The uncomfortable point is this: the FCA can help, but it cannot reverse every scam. Victims need to move quickly, report to the right organisations, preserve evidence and understand which route may apply to their case.

What The FCA Can And Cannot Do For Scam Victims

The FCA is the UK regulator for financial services firms and financial markets. It authorises and supervises firms, sets conduct rules, issues warnings about unauthorised businesses, and can take enforcement action where firms or individuals break financial services rules. That gives it real power, but not unlimited power.

For scam victims, the FCA’s first useful function is information. The FCA provides consumer guidance on how to spot scams, how to check firms, and how to report suspicious contact. Its protect yourself from scams guidance tells consumers to report potential scams to the FCA and, where money has been lost or the matter falls outside FCA regulation, to contact Report Fraud. That distinction matters because victims often assume there is one single office that handles everything. There is not. Welcome to public administration, bring a flask.

The FCA can use reports from victims to identify unauthorised firms, publish warnings, investigate patterns, work with other agencies, and stop more people being caught. That is valuable, even if it does not feel satisfying to someone who has just lost savings. A report may not produce instant recovery, but it can help build the evidence trail around a scam operation.

The FCA also provides the FCA Warning List, which allows consumers to search for unauthorised firms and individuals that the regulator is aware of. This is especially useful in investment, trading, pension, crypto and clone firm scams. If the name, website, phone number or email appears on the list, that is a serious warning.

But the FCA cannot usually get money back from a criminal scammer. If a victim sent money to an unauthorised firm, fake broker or overseas fraud operation, recovery may depend on the bank, payment provider, police, insolvency process, civil action, or whether the funds can be traced and frozen. The FCA does not provide compensation simply because a person has been scammed.

The FCA also cannot help with every product that looks financial. Some scams involve cryptoassets, overseas entities, fake apps, fake job offers, romance fraud, social media impersonation, commodity schemes, or unregulated investments. The FCA may still want reports where financial services are being misrepresented, but the victim may also need to report to police services, banks, payment firms and other agencies.

A practical way to view the FCA is as the regulator and intelligence point, not the refund desk. It helps victims understand whether a firm was authorised, whether it may be a clone, how to report the scam, and which formal routes might exist for complaints or compensation. That is not everything, but it is still useful when the alternative is arguing with a fake “account manager” who has suddenly discovered three new withdrawal fees.

The First Steps After A UK Investment Scam

The first step after suspecting a scam is to stop paying. That sounds obvious, but many victims continue because the scammer says the account can still be released. There may be a tax fee, upgrade fee, compliance charge, insurance bond, anti money laundering payment, wallet activation cost, or “final clearance” fee. The names change. The aim does not. More payments usually mean more loss.

The second step is to contact the bank, card provider, payment app, exchange or payment service used to send the money. Speed matters. If the payment was recent, the provider may be able to stop, recall, freeze, dispute or flag it. If the scam involved an authorised push payment, where the victim was tricked into sending money from their account, the bank or payment provider may have specific obligations under the UK’s reimbursement regime.

The third step is to preserve evidence. Victims should save account dashboards, emails, text messages, WhatsApp chats, Telegram messages, call logs, websites, payment instructions, wallet addresses, transaction references, bank details, names used, company numbers, supposed FCA numbers and screenshots of trading balances. Fraud websites disappear. Chat accounts get deleted. Sales agents go from chatty to ghost faster than a bad penny stock.

The fourth step is to check the firm. The FCA Firm Checker helps consumers see whether a financial services firm is authorised by the FCA and has permission to provide the relevant products or services. This is not just a box ticking exercise. It can affect which recovery options are available. Dealing with an authorised firm may open complaint and compensation routes that do not exist with a completely unauthorised scam.

The fifth step is to report the matter. For England, Wales and Northern Ireland, the main police reporting route is Report Fraud, the UK reporting service for fraud and cyber crime. The GOV.UK page on reporting online scams and phishing directs people who have lost money or been hacked through an online scam in England or Wales to Report Fraud, and says victims in Scotland should report to Police Scotland.

Victims should also report the scam or unauthorised firm to the FCA where the scam involves financial services, investments, trading platforms, pensions, insurance, loans, claims management or regulated sounding activity. The FCA’s report a scam page explains how to report scams and unauthorised firms to the regulator.

These steps do not guarantee recovery. They do increase the chance of stopping further loss, creating a proper record, and getting the case into the right system. In scam cases, delay is expensive. Silence is even more expensive.

One of the FCA’s most practical roles is helping victims identify what kind of firm they were dealing with. This matters because scams often rely on confusion between authorised firms, unauthorised firms and cloned firms.

An authorised firm is a business that has permission from the FCA to carry out regulated financial activities. It may still behave badly, and it may still receive complaints, but it is inside the regulatory perimeter. That means consumers may have access to complaints processes, the Financial Ombudsman Service, or compensation arrangements if the firm fails and the claim is eligible.

An unauthorised firm is different. It may be selling financial products or services in the UK without permission. If a person deals with an unauthorised firm, FCA protections are usually much weaker. The victim may not be able to use the Ombudsman or FSCS for losses caused by that unauthorised business. This is why checking before depositing matters so much. After the event, the answer can be grim.

A clone firm is nastier. It copies the details of a real authorised firm to trick consumers. It may use the same name, a similar website, a real firm reference number, and stolen branding. The victim searches the name, sees a real FCA entry, and assumes everything is safe. The problem is that the phone number, email, website or payment account belongs to the fraudster.

The FCA Financial Services Register is the public record of firms, individuals and bodies that are, or have been, authorised by the FCA or PRA. Victims can use it to compare the details they were given with the official details held by the regulator. The comparison needs to be precise. Similar is not enough. A scammer needs only one convincing mismatch to steal trust.

The FCA’s Warning List of unauthorised firms also helps by listing firms and individuals the FCA knows are operating without authorisation. If the suspect firm appears there, victims should stop dealing with it and report the details. If it does not appear, that does not prove safety. A scam may simply not have been reported yet.

This is where the FCA helps victims turn a confusing situation into categories. Was the firm authorised? Was it a clone? Was the activity regulated? Was the product outside the FCA’s perimeter? Was the victim dealing with a payment scam rather than an investment firm? These distinctions influence the next step.

For example, if the victim was tricked into transferring money to a fake investment account, their first recovery route may be the bank under authorised push payment rules. If they dealt with an authorised financial adviser who gave unsuitable advice and the firm later failed, FSCS might become relevant. If an authorised bank refused a scam reimbursement unfairly, the Ombudsman may be relevant. If the money went to a criminal overseas wallet, the police reporting route becomes central, though recovery may still be difficult.

The FCA does not remove the pain of the loss. It helps define the problem, and in scams, defining the problem correctly is not academic. It can decide where the victim should spend their next hour.

Reporting Scams Through FCA, Report Fraud And Police Scotland

Reporting a scam in the UK usually involves more than one organisation. That can feel irritating at the exact moment a victim needs simplicity, but each body has a different job.

The FCA wants reports about scams involving financial services, unauthorised firms and suspicious investment activity. Its report a scam service lets consumers tell the regulator about a suspected scam or unauthorised firm. The FCA may use that information to issue warnings, support supervisory work, investigate misconduct or share intelligence with law enforcement.

Report Fraud is the police reporting route for fraud and cyber crime in England, Wales and Northern Ireland. The Report Fraud reporting guide says reports can be made online at any time and that advisers are available to give help and advice. This matters because investment scams often cross into cyber crime through fake websites, spoofed emails, remote access software, phishing and identity theft.

For Scotland, the route is different. The FCA’s consumer guidance and the GOV.UK scam reporting page direct victims in Scotland to Police Scotland, normally through 101, when money has been lost to a scam. That difference should not be ignored. UK wide does not always mean one reporting route for everyone. Because apparently fraud was not already administratively fiddly enough.

Victims should report even if they feel embarrassed or believe the money is gone. Reports help identify criminal networks, connect cases, support warnings, and help agencies understand scam methods. A single report may look small. Hundreds of similar reports can show a pattern.

The National Cyber Security Centre is also relevant where the scam involved phishing emails, fake websites or suspicious messages. The NCSC’s phishing and scam reporting guidance explains how suspicious emails can be forwarded to report@phishing.gov.uk and suspicious texts can be forwarded to 7726. The NCSC can use reports to help remove malicious sites and reduce harm to others.

A strong report should be factual and organised. It should include names used by the scammer, website addresses, email addresses, phone numbers, payment details, dates, amounts, account numbers, crypto wallet addresses, transaction IDs, screenshots, contracts, promotional material and any claim that the firm was FCA authorised. Emotional detail can matter too, but the first job is evidence.

Victims should also keep the report numbers. Banks, insurers, legal advisers, the Ombudsman and other bodies may ask for them later. A clear paper trail makes the next stage easier. It also stops the victim from having to reconstruct everything from memory, which is a miserable hobby and not recommended.

Getting Money Back Through Banks, FSCS And The Ombudsman

The FCA may help direct victims, but the route to getting money back often runs through banks, payment providers, the Financial Services Compensation Scheme, or the Financial Ombudsman Service.

For payment scams, especially authorised push payment scams, the victim’s bank or payment provider is often the first recovery route. Authorised push payment fraud happens when a person is deceived into sending money to a fraudster. From 7 October 2024, the Payment Systems Regulator’s APP scams reimbursement requirement introduced mandatory reimbursement protections for eligible APP scam payments through Faster Payments, with a maximum reimbursement level. The PSR’s later consolidated policy statement confirms that reimbursable Faster Payments or CHAPS APP scam payments made on or after 7 October 2024 are covered by the regime.

That does not mean every victim is automatically refunded. Eligibility, timing, payment type, consumer behaviour and exceptions matter. But victims should contact their bank quickly and make a formal scam claim. They should explain what happened, provide evidence, and ask the bank to assess reimbursement under the relevant rules.

If the bank refuses reimbursement or handles the case poorly, the victim may be able to complain. The GOV.UK guidance on complaining about a financial service explains that consumers should follow the firm’s complaints procedure and may usually take the complaint to the Financial Ombudsman Service if unhappy with the response.

The Financial Ombudsman Service fraud and scams page explains how consumers can bring complaints about the way a bank or payment services provider acted when they were scammed or became a victim of fraud. The Ombudsman is not the police. It does not chase criminals. It looks at whether the financial business treated the customer fairly and followed relevant rules.

This can be important where a bank ignored warning signs, failed to intervene, rejected a claim unfairly, mishandled a complaint, or did not apply scam reimbursement rules correctly. The Ombudsman can tell a firm to put things right where it upholds a complaint. For victims who feel blocked by a bank’s first response, this route can matter.

The FSCS is different again. The Financial Services Compensation Scheme protects customers when authorised financial services firms fail and cannot pay valid claims. It is free to claim directly through FSCS. Its protection can apply in certain cases involving deposits, investments, insurance, pensions, mortgage advice and other regulated activities, but eligibility depends on the firm, product, activity and circumstances.

The FCA’s own guidance on claiming compensation when a firm fails explains that consumers may be able to claim compensation if a financial firm has gone out of business and owes them money. This is not the same as compensation for sending money to a random unauthorised scammer. The firm usually needs to have been authorised and the claim must fall within FSCS rules.

This distinction is where many victims get disappointed. If a fake investment platform pretended to be FCA regulated but was not, FSCS protection may not apply. If a real authorised adviser gave bad regulated advice and then failed, FSCS may be relevant. The facts decide the route.

Victims should be cautious with paid claims management companies and recovery services. FSCS says its service is free, and consumers who claim directly keep all compensation owed to them. Anyone promising guaranteed recovery from a scam for an upfront fee should be treated with care. Recovery scams are common because fraudsters know victims are desperate to reverse the loss. It is grim, but criminals are not famous for stopping at one bite.

The best recovery path often uses several channels at once: report to the bank, report to the FCA, report to Report Fraud or Police Scotland, preserve evidence, complain formally where a regulated firm is involved, and escalate to the Ombudsman if needed. It is not elegant. It is the system victims have.

How FCA Warnings Help Other Investors

When victims report scams to the FCA, the benefit is not always personal or immediate. Sometimes the main effect is public protection. That may feel thin when money has gone, but it still matters.

The FCA can add firms to its Warning List, publish consumer alerts, identify clone firms, and share information with other authorities. A warning can stop future victims from depositing money. It can also help banks, search engines, platforms and other institutions recognise suspicious activity.

FCA warnings also help consumers check contact details. In clone firm cases, warnings often identify the fake website, phone number, email address or trading name being used by scammers. That is useful because the fraudster’s strongest weapon is confusion. A warning reduces that confusion.

The FCA’s work also has a deterrent effect against authorised firms. Regulated businesses know that the FCA expects systems and controls around financial crime, customer protection and fair treatment. In October 2024, the FCA sent a Dear CEO letter on APP fraud reimbursement expectations to payment and e-money institutions, linking APP fraud to its wider financial crime priorities. That matters because scam prevention is not only about telling consumers to be careful. Firms also need to design better controls.

The public warning function is also why victims should report even after accepting that recovery is unlikely. A scam that is not reported stays quieter for longer. A scam that appears in enough reports becomes easier to expose.

There is no need to romanticise this. A warning list does not stop every fraudster. Criminals change names, domains, phone numbers and scripts. But warnings raise the cost of the scam and give future investors something concrete to find. In fraud prevention, concrete beats vibes.

Practical Prevention Before The Next Approach

The best time to use FCA tools is before sending money. That is not comforting to someone already scammed, but it is important for everyone else.

A UK investor should check the firm through the FCA Firm Checker and the Financial Services Register. They should compare the firm name, reference number, permissions, website, phone number and email address. They should not rely on links sent by the salesperson. They should find the register independently.

They should also search the Warning List. Absence from the list is not proof of safety, but presence on it is a serious problem. If a firm is listed as unauthorised or cloned, the investor should stop contact and report any approach.

The payment route should match the firm. Money should not be sent to personal accounts, unrelated businesses, overseas wallets, gift cards, or payment apps because an “account manager” says it is faster. Faster is not safer. It is often just faster at becoming your worst bank statement line.

Investors should question guaranteed returns, pressure tactics, secrecy, bonus traps, celebrity endorsements, social media pitches, and recovery offers. A real financial firm can answer written questions. A real investment can explain risk. A real adviser can be checked. A scammer pushes emotion because facts are inconvenient.

Victims of previous scams should be especially careful. Their details may be sold or reused. Follow up recovery scams often claim to be lawyers, regulators, blockchain analysts, police contacts or FCA agents. The FCA will not ask for a payment to release recovered funds. Anyone making that kind of demand should be treated as a fresh threat, not a solution.

Final Warning

The FCA helps UK scam victims by giving clear reporting routes, maintaining public registers, warning about unauthorised firms, supporting enforcement and directing consumers towards the right recovery channels. That help is real, but it has limits.

Money recovery usually depends on the payment route, the firm’s authorisation status, the bank’s response, FSCS eligibility, Ombudsman decisions, police action and the quality of evidence. The FCA is not a magic refund button.

For traders and investors, the practical lesson is plain. Check before funding. Report quickly after suspicion. Preserve evidence. Use official routes. Ignore anyone asking for another payment to release money.

A scammer wants speed, silence and confusion. The FCA system works best when victims do the opposite: slow down, document everything and report through the proper channels.